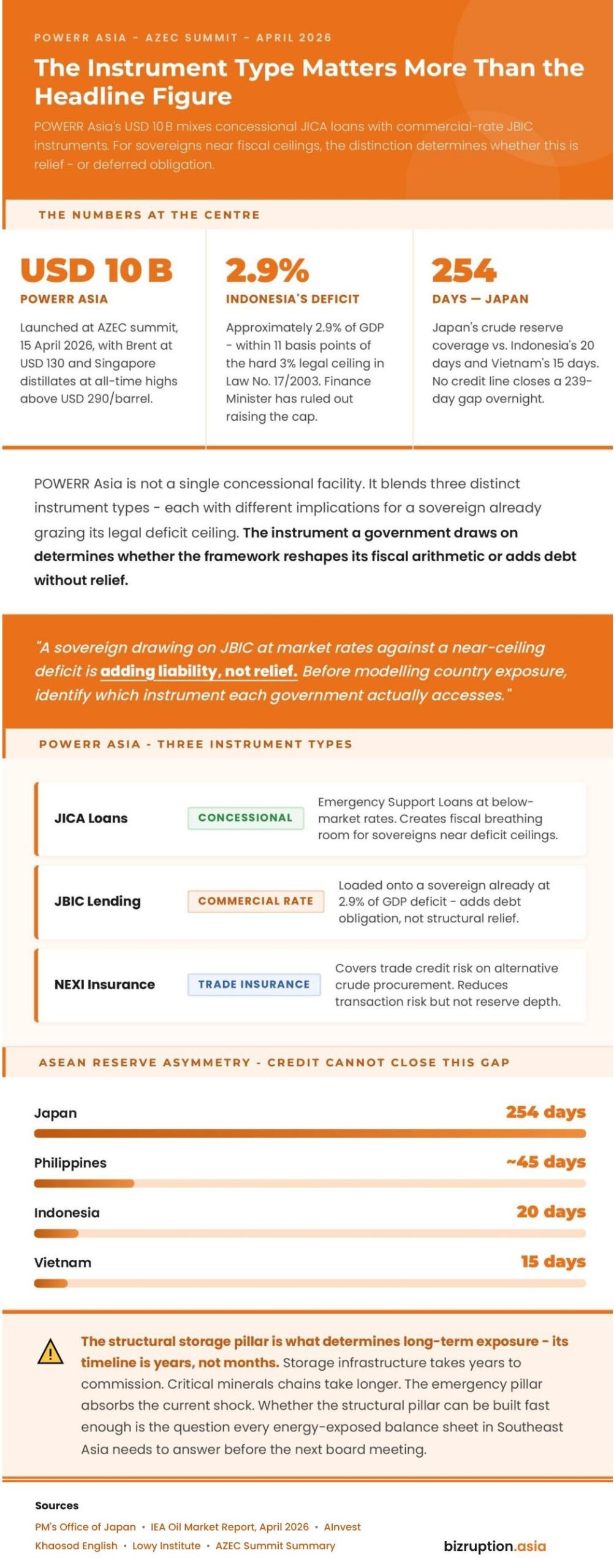

At the 15 April AZEC summit in Tokyo, Japanese Prime Minister Sanae Takaichi launched POWERR Asia – a USD 10 billion framework to stabilise Asia’s energy supply chains – with Brent crude at USD 130 per barrel and Singapore middle distillates hitting all-time highs above USD 290 per barrel. The scale of Japan’s response is not in question. The mechanism is.

POWERR Asia – Partnership on Wide Energy and Resources Resilience – is not a single concessional facility. Japan’s official framework blends JICA Emergency Support Loans at concessional rates with commercial-rate JBIC lending, NEXI trade insurance and ADB co-financing.

For a sovereign already in fiscal distress, that distinction is the whole argument. A soft loan creates breathing room. A commercial credit line defers the obligation.

The Reserve Gap That Credit Lines Cannot Fill

The structural problem predates the announcement by years. Indonesia holds 20 days of crude reserves. Vietnam holds 15. Japan – the architect now offering to finance the region’s oil procurement – holds 254. That gap is not a policy failure. It is a physical infrastructure deficit: storage tanks, release systems and the capital to build them, none of which a credit line delivers overnight.

The Philippines imports 98% of its crude from the Middle East. Petrol prices have jumped 76% since Hormuz closed on 28 February 2026. Indonesia consumes 1.5 million barrels per day against domestic output below 700,000. Each USD 1 rise in oil forces an additional IDR 10.3 trillion onto Indonesia’s subsidy bill – a bill built on a USD 70 per barrel assumption that no longer exists.

The fiscal math is now brutal. Indonesia’s deficit sits at approximately 2.9% of GDP, within reach of the 3% hard ceiling in Law No. 17/2003. Finance Minister Purbaya Yudhi Sadewa has ruled out raising that ceiling. The government is cutting spending across ministries. Infrastructure programmes go first.

The Safety Net That Has Never Been Tested

At the same summit, Philippine President Ferdinand Marcos Jr. delivered the meeting’s most revealing moment. He called for immediate activation of the ASEAN Petroleum Security Agreement (APSA) and offered Manila as host of its first emergency simulation exercise. His message was blunt: “The mechanism exists and it should be tested now.”

APSA has been on the books since 1986, updated in 2009, renewed in October 2025. It has never been activated. Sharing is voluntary and done at commercial rates; meaning a country in distress still pays market price for any barrels it receives. At USD 130 per barrel, that is not a relief mechanism. It is a procurement channel with a regional letterhead.

Marcos understood the gap: “No single country in Asia can insulate itself from supply chain shocks of this scale,” he told the same summit.

What the Framework Actually Buys

POWERR Asia has two pillars. The emergency pillar finances procurement of alternative crude – including US barrels – and extends credit across Japan’s regional supply chain. The structural pillar funds storage construction, LNG diversification, biofuels, small modular reactors and critical minerals sourcing.

The structural pillar carries the lasting value. It also carries the longest lag. Storage infrastructure takes years to commission. Critical minerals chains take longer. Takaichi was direct after the talks: “Supporting Asian countries’ supply chains would in turn bolster Japan’s own economy.”

This is regional solidarity, yes, but it is also supply-chain self-insurance for Tokyo.

The Lowy Institute put it cleanly: “ASEAN’s current approach to resilience absorbs shocks rather than reducing exposure to what causes them.” The emergency pillar is absorption. The structural pillar is the first credible attempt at exposure reduction. The gap between the two is measured in years of investment, not months of credit.

The geopolitical positioning is not subtle. Tokyo is anchoring itself to ASEAN’s energy architecture at the precise moment Washington caused the Hormuz closure and Beijing – which Iran continues to allow passage – sits on 200 days of reserves, unmoved.

The Instrument That Determines the Outcome

For a CIO pricing sovereign risk across Southeast Asia or a CFO stress-testing project costs against sustained USD 130 crude, the question is not whether POWERR Asia exists. It is which instrument their government draws on.

A JICA concessional loan reshapes fiscal arithmetic. A JBIC commercial credit line, loaded onto a sovereign already grazing its legal deficit ceiling, adds debt without relief.

Lawrence Wong’s, Anwar Ibrahim’s and Prabowo Subianto’s governments all welcomed the framework on 15 April. None has specified tranche size or instrument mix. That specification – due from Japan’s implementing agencies – is the number that determines whether POWERR Asia is a structural intervention or an expensive bridge to the same problem.

The IEA’s April 2026 Oil Market Report offers two scenarios: a short-term disruption or prolonged constraint. Japan’s $10 billion is sufficient for the former. In a prolonged scenario, the effectiveness of the framework depends on how quickly structural measures come online.

The structural pillar hedges the second. Whether it can be built fast enough is the question every energy-exposed balance sheet in Southeast Asia needs to answer before the next board meeting, not after it.

FIVE NUMBERS EVERY CIO AND CFO IN SOUTHEAST ASIA NEEDS RIGHT NOW

239 days — The reserve gap between Japan (254 days of crude coverage) and Indonesia (15 days) that no credit line closes overnight. Vietnam sits at 15 days. The Philippines has drawn down from 55–57 days at crisis onset to approximately 45 days as of late March 2026. Reserve depth is the single most predictive variable for sovereign energy stress duration. Sources: Khaosod English, Nation Thailand, Wikipedia/Philippine energy crisis page citing DOE

IDR 10.3 trillion — Additional fiscal spending Indonesia absorbs for every USD 1 increase in the oil price. The 2026 energy subsidy budget was built on USD 70 per barrel. Brent is near USD 130. That is a USD 60 gap, compounding in real time against a deficit already at approximately 2.9% of GDP — within 11 basis points of the 3% hard ceiling in Law No. 17/2003. Source: AInvest, citing Indonesian budget data

USD 290 per barrel — The all-time high Singapore middle distillate crack reached in April 2026, per the IEA’s April Oil Market Report. For any corporate with energy costs as a percentage of operating expenditure — shipping, aviation, manufacturing, logistics — this is the number repricing every contract written before 28 February 2026. Source: IEA Oil Market Report, April 2026

USD 10 billion across three instrument types — POWERR Asia is not a single concessional facility. It blends JICA Emergency Support Loans (concessional), JBIC lending (commercial rate) and NEXI trade insurance. A sovereign drawing on JBIC at market rates against a near-ceiling deficit is adding liability, not relief. Before modelling country exposure, identify which instrument each government actually accesses. Source: POWERR Asia Overview, Prime Minister’s Office of Japan

Every USD 10 per barrel — cuts Philippine GDP growth by approximately 0.2 percentage points and raises inflation by approximately 0.6 percentage points, per MUFG Research. At sustained USD 130 per barrel, MUFG estimates Philippine GDP growth falls to approximately 3.4% in 2026 — more than 1.5 percentage points below pre-crisis consensus. Replicate this sensitivity across Indonesia, Vietnam and Thailand for any portfolio with ASEAN sovereign or corporate exposure. Source: MUFG Research, Philippines Strait of Hormuz Impact, 9 March 2026

References:

- POWERR Asia Overview — Prime Minister’s Office of Japan, 15 April 2026

- AZEC Plus Online Summit Summary — Prime Minister’s Office of Japan, 15 April 2026

- Oil Market Report — International Energy Agency, April 2026

- Japan Plans USD 10 Billion Framework to Help Asia Secure Oil — MarketScreener/Reuters, 15 April 2026

- Asian Nations Oil Reserves Under Spotlight — Khaosod English, 4 March 2026

- Asian Nations Assure Energy Supplies — Nation Thailand, 4 March 2026

- Marcos Urges ASEAN to Activate Fuel-Sharing Pact — Interaksyon/Philstar, 15 April 2026

- Marcos Pushes Unified Asia Response to Energy Crisis — Manila Bulletin, 15 April 2026

- ASEAN States Working on Fuel-Sharing Deal — Inquirer Global Nation, 17 March 2026

- Indonesia’s Fiscal Liquidity Crunch — AInvest, April 2026

- Navigating Oil Shock: Fiscal Challenges for Indonesia — The Jakarta Post, 31 March 2026

- ASEAN’s Energy Crisis Is Not About Energy — Lowy Institute, April 2026

- 2026 Strait of Hormuz Crisis — Wikipedia (citing IEA, Kpler, Reuters), updated April 2026

{kind=link}