On 23 March 2026, Executive Secretary Ralph Recto stood at Malacanang and set the target: USD 110 billion in Philippine semiconductor and electronics exports by 2030, up from roughly USD 45 billion today, achieved by moving the country from assembly and testing into integrated circuit design and wafer fabrication.

An unambiguous pitch to US capital. That same week, the Bangko Sentral ng Pilipinas published what that capital had actually been doing. Net FDI inflows into the Philippines in 2025: USD 7.79 billion. A 17.1% drop. The lowest since 2015, pandemic years excluded.

Two numbers. One pitch, one verdict. The distance between them is where the investment decision lives.

The BOI Says Record. The BSP Says Decade Low. Both Are Right

Here is what every Philippines investment pitch deck leads with: the BOI approved PHP 1.56 trillion in investments in 2025 – the second-highest in the agency’s 58-year history.

Here is what none of them mention: the BSP stated explicitly in its March 2026 release that its figures measure actual capital flows, while BOI figures measure commitments to investment promotion agencies. Commitments that go undeployed do not cross the border.

The USD 7.79 billion that did cross tells its own story. The full-year 2025 decline was concentrated – a 27% collapse in debt instruments, specifically intercompany borrowings between foreign investors and their Philippine subsidiaries, to USD 5.27 billion, while equity placements and reinvested earnings both rose.

By January 2026, however, net FDI fell a further 39.2% year-on-year to USD 0.4 billion, with declines across all components – equity capital, reinvested earnings, and debt instruments – as the BSP attributed the contraction to geopolitical risk and the Hormuz-driven commodity shock.

Those headwinds hit every market in the region. Vietnam’s disbursed FDI rose 9% in the same period to USD 27.62 billion, a five-year high. The Philippines fell to a decade low. Same conditions. Different outcomes.

The roadmap and the flows are measuring different realities. Any five-year model needs both.

What Manila Is Actually Selling and Why Washington Is Buying

The foundation behind the Philippines semiconductor pitch is real, not projected. Electronic products – semiconductors dominant among them – generated USD 41.91 billion in export revenue in the first 11 months of 2025, up 15.5% year-on-year, per the Philippine Statistics Authority; SEIPI projects the full-year figure at USD 48–49 billion.

Bataan, Laguna, and the Clark corridor host assembly, testing and packaging operations for US firms whose Philippine output feeds directly into American supply chains. The country ranks ninth globally in chip exports and holds roughly 5% of the global semiconductor market, all of it in the back end of the value chain: lower-margin, technically essential, and deeply embedded.

Washington is not buying on sentiment. On 17 April 2026, Under Secretary of State Jacob Helberg announced at the US Embassy in Manila that the United States and the Philippines would establish a 4,000-acre industrial hub in the Luzon Economic Corridor – the first AI-native Economic Security Zone under Pax Silica, a 14-nation supply chain security framework.

The alliance advantage is now US State Department policy.

So is the contingency. President Trump’s August 2025 announcement of a potential 100% semiconductor tariff – with carve-outs only for companies manufacturing in the US or committed to doing so – introduced a scenario no Section 232 exemption forecloses.

That exemption currently shields Philippine semiconductor exports from the 19% US reciprocal tariff. It holds by executive determination, not treaty. Allocators modelling decade-long payback periods cannot price it as permanent.

Why the CREATE MORE Act Does Not Yet Close the Gap Against Vietnam and Malaysia

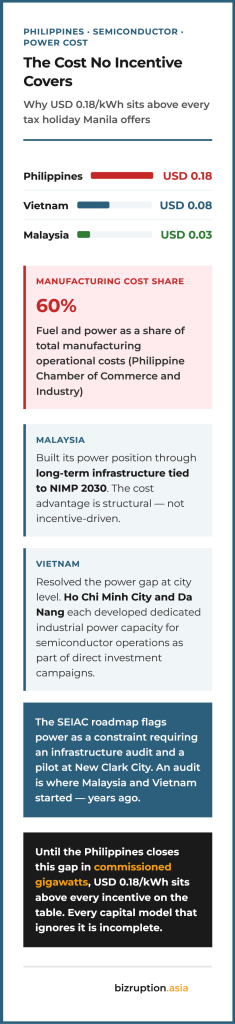

The single most important fact in the Philippines semiconductor investment case is not in the SEIAC roadmap. It is in the power bill.

Industrial electricity in the Philippines costs USD 0.18 per kWh – confirmed at a congressional hearing and reported by the Philippine News Agency. Vietnam: USD 0.08. Malaysia: USD 0.03. The Philippine Chamber of Commerce and Industry calculates that fuel and power account for 60% of manufacturing operational costs nationwide.

Semiconductor fabrication runs continuous, high-load, 24-hour operations. No tax incentive closes a six-times cost gap on the input that defines the operating structure.

The CREATE MORE Act, signed by Marcos in November 2024, compounds the problem by omission. The law offers a Special Corporate Income Tax of 5% or an Enhanced Deduction Regime at 20% CIT, with periods of 17 to 27 years, but it contained no specific semiconductor provision.

The Presidential Advisory Council flagged the gap and recommended a revision to the implementing rules. That revision is ongoing.

Vietnam and Malaysia moved earlier and with sharper instruments. Vietnam’s CIT Law 2025, effective 1 October 2025, explicitly names semiconductor chip research, design, production, packaging and testing as priority activities: 10% CIT for 15 years, four years fully exempt, nine years at half-rate, plus R&D subsidies covering up to 50% of initial investment through Decree 182/2024. Project approval timelines in special semiconductor zones were cut by 250 to 300 days.

Malaysia’s NIMP 2030 deploys Investment Tax Allowances of 60%-100% of qualifying capital expenditure, dedicated IC design export incentives and a MYR 200 million Innovation Commercialisation Fund – against an electricity tariff of USD 0.03 per kWh.

The Philippines is chasing the same capital with a blunter incentive, a higher power cost and a semiconductor-specific framework still being drafted.

The One Thing the Philippines Semiconductor Roadmap Got Right

Recto did not oversell. At the March SEIAC meeting, he directed implementation to carry clear deadlines and assigned responsibilities, and stated plainly: “Otherwise, it is just paper with ambition printed on it.” Previous Philippine industrial roadmaps collapsed on exactly that standard. The candour tells investors precisely where to apply due diligence pressure which is more useful than optimism.

The assembly and testing base is secure. Washington is paying for proximity to it. But the path to USD 110 billion runs through a power tariff no incentive neutralises and a tax framework with a semiconductor-sized hole still open. Investors who price that gap before Recto’s deadlines arrive – not after they miss – will not be reading the next BSP FDI release with surprise.

References:

- Philippine Semiconductor Roadmap, USD 110 Billion Target – SEIAC Malacañang Meeting

- BSP Full-Year 2025 Philippines FDI Net Inflows, USD 7.79 Billion, 17.1% Decline – BSP Primary Release, reported by Manila Bulletin

- BSP Confirmation: FDI Covers Actual Flows, BOI Covers Commitments – Manila Standard

- BSP Philippines FDI January 2026, 39.2% Year-on-Year Decline, All Components Down – BSP via Trading Economics

- PSA Electronic Products Exports USD 41.91 Billion, January-November 2025, Up 15.5% – PSA via Manila Bulletin

- SEIPI Full-Year 2025 Electronics Export Projection USD 48-49 Billion – Manila Bulletin

- BOI Full-Year 2025 Investment Approvals, PHP 1.56 Trillion – BusinessWorld

- CREATE MORE Act, No Semiconductor Provision – BusinessWorld / PIDS

- SEIAC Implementation Directives, Recto Quote – Manila Bulletin

- Recto Quote Confirmed Verbatim – “Otherwise, it is just paper with ambition printed on it” – NewsBytesph / DTI

- US–Philippines 4,000-Acre Economic Security Zone, Luzon Economic Corridor, Pax Silica – US Department of State Primary Release

- US Embassy Manila Fact Sheet – Helberg Statement, Pax Silica

- Section 232 Semiconductor Tariff Exemption, Philippines – Philstar

- Philippines Industrial Electricity USD 0.18/kWh vs ASEAN – Philippine News Agency

- Vietnam CIT Law 2025, Semiconductor-Specific Incentives – Alvarez & Marsal

- Vietnam Decree 182/2024, Investment Support Fund, R&D Subsidy Up to 50% – Deloitte Southeast Asia

- Vietnam Law on Investment Amended, Semiconductor Approval Shortened 250–300 Days – Acclime Vietnam

- Malaysia NIMP 2030 ITA Incentives, IC Design Export Benefits, MYR 200 Million Fund – PWC Tax Summaries Malaysia

- Vietnam Disbursed FDI USD 27.62 Billion, Up 9%, Five-Year High – Vietnam Foreign Investment Agency via VIR

- IMF Philippines Article IV Consultation

{kind=link}