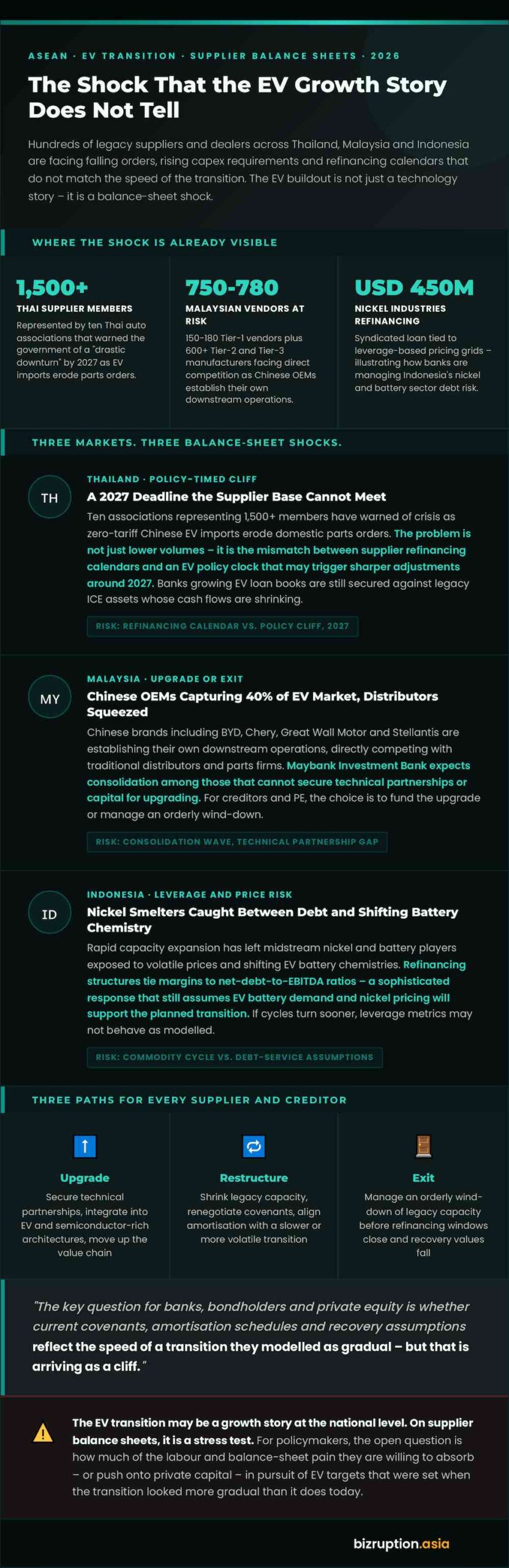

Ten Thai automotive associations warned in May 2026 that the sector could face a “drastic downturn” by 2027 as EV adoption erodes domestic production and parts orders. Malaysia’s policymakers openly talk about traditional auto part suppliers needing to upgrade or risk being phased out.

Indonesia’s nickel and battery boom is already exposing smelters and midstream players to price risk and leverage mismatches. The EV buildout is not just a technology story; it is a balancesheet shock.

This analysis looks at where that shock is landing and what it means for creditors, private equity and policymakers across the region.

Thailand’s Suppliers Face a PolicyTimed Cliff, Not a Gentle Slope

Thailand is the clearest case of the shock arriving faster than supplier assumptions. Ten Thai auto and parts associations, representing more than 1,500 members, have warned the government that the sector is heading toward crisis as cheap, zerotariff EV imports from China erode local production and parts orders.

Their letter explicitly links the risk to the expiry of EV incentive programmes around 2027 – the point at which factories and suppliers that retooled late may find themselves without a policy backstop.

The credit story is equally important. Thai banks and autoloan providers are actively growing EV portfolios – Krungsri Auto and TMBThanachart Bank both expect EV loans to be a key growth driver while keeping NPLs under 1%.

That supports demand for new vehicles and indirectly, new EValigned supply chains. But the assets securing those loans still include legacy ICE vehicles, dealerships and supplier exposures whose cash flows depend on a production base that industry groups say is shrinking under competitive pressure.

For creditors and PE owners of Thai suppliers, the problem is not just lower orders; it is the mismatch between refinancing calendars and an EV policy clock that may trigger sharper adjustments around 2027.

Malaysia’s Vendors and Distributors Must Choose Between Upgrading and Exit

Malaysia’s supplychain risks look different but are no less real. The country still has 150-180 Tier1 vendors and more than 600 Tier2 and Tier3 components manufacturers serving national marques and foreign OEMs. As

Deputy Investment Minister Sim Tze Tzin has noted, the government wants foreign manufacturers to collaborate with local vendors to “move up the value chain” and prepare them to become exportoriented suppliers of sensors, chips and software.

UNCTAD’s analysis of Malaysia’s EV transition similarly emphasises the need for technical upgrading and integration into highervalue segments of the EV supply chain. Yet the pressure is already visible.

Industry coverage shows Chinese EV brands capturing close to 40% of Malaysia’s EV market, with traditional distributors and parts suppliers facing direct competition from OEMs like BYD, Chery, Great Wall Motor and Stellantis as they establish their own downstream operations.

Maybank Investment Bank expects this to drive consolidation among local distributors and parts firms, pushing those that cannot secure technical partnerships or capital for upgrading towards exit.

For creditors and PE owners, the choice is stark: fund upgrading and integration into EV and semiconductorrich architectures or manage an orderly winddown of legacy capacity.

Indonesia’s Battery and Nickel Players Carry Leverage and Price Risk

Indonesia’s suppliers sit higher up the EV chain, but their balancesheet challenges are no less acute. RIETI’s mapping of the ASEAN EV market and related work on Indonesia’s nickel and battery sector show that rapid capacity expansion has left some smelters exposed to volatile nickel prices and shifting battery chemistries.

As price cycles turn and demand forecasts are revised, midstream players with debtfunded capacity can find themselves squeezed between offtake commitments and weaker margins.

Recent refinancing deals – such as Nickel Industries’ USD 450 million syndicated loan package led by Bank Negara Indonesia and tied to leveragebased pricing grids – illustrate how banks are attempting to manage this risk by linking margins to netdebttoEBITDA ratios and aligning amortisation schedules with project rampup.

That is a sophisticated response, but it still assumes that EV battery demand and nickel pricing will support the planned transition from stainlesssteel grade output to batteryrelated products. If the transition is slower or more volatile than expected, leverage metrics may not behave as modelled.

The Credit and Policy Question That EV Narratives Do Not Answer

Across Southeast Asia, the EV transition is forcing suppliers and creditors to choose between three paths: upgrade into the new supply chains, restructure and shrink, or exit.

Thailand’s suppliers face a policytimed cliff around 2027; Malaysia’s vendors must secure technical partnerships or risk being outcompeted; Indonesia’s midstream players carry leverage tied to volatile commodity and technology cycles.

For banks, bondholders and private equity, the key question is whether current covenants, amortisation schedules and recovery assumptions reflect this reality. For policymakers, the question is how much of the labour and balancesheet pain they are willing to absorb – or push onto private capital – in pursuit of EV targets.

The EV transition may be a growth story at the national level. On supplier balance sheets, it is a stress test.

References:

- Thai auto sector facing crisis unless EV policy is overhauled, industry groups warn – Reuters

- Thailand Ends 2024 with Sales and Manufacturing Slumps – AfMA

- IFC subscribes to first green bond issued by TMBThanachart Bank focused on electric vehicles – IFC

- Malaysia Targets Stronger EV Ecosystem Via OEM-Local Vendor Ties – Bernama

- New auto landscape emerging in Malaysia as Chinese EV brands make inroads – TheSun

- Electric Vehicle Transition in Malaysia – UNCTAD

- EV Market in ASEAN: Policies, Current Status & Framework – RIETI

- Indonesia’s Nickel Boom Leads to Smelter Shutdowns – Discovery Alert

- Nickel Industries secures US$450M refinancing to fuel EV battery growth – Grafa

{kind=link}