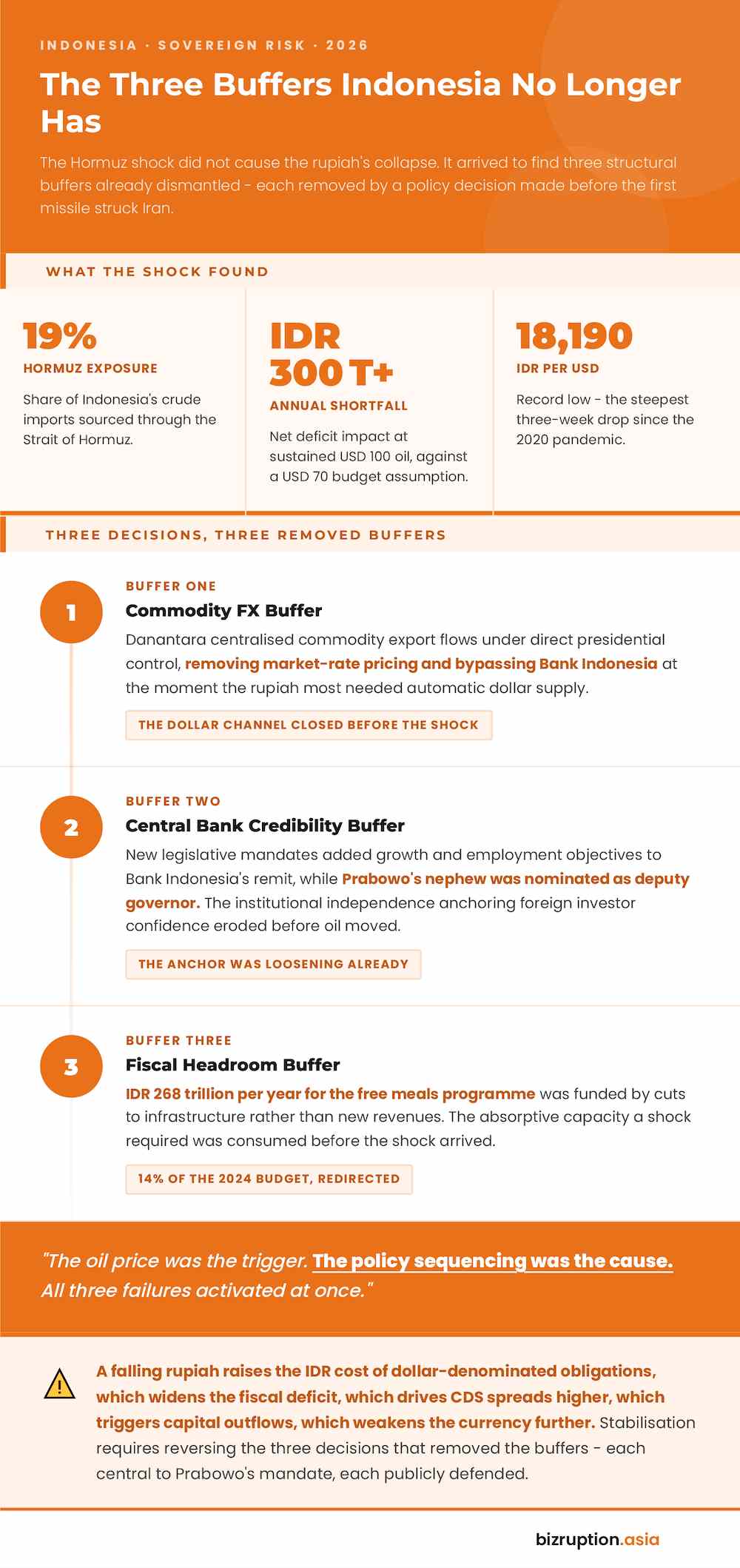

Indonesia’s credit default swaps are pricing a loss of investment-grade status. The rupiah is at IDR 18,190 – a record low. The Jakarta Composite is the world’s worst-performing major equity index in 2026, down 42%. The Hormuz closure contributed to all three. It caused none of them.

Three policy decisions, each taken before the first US-Israeli missile struck Iran on 28 February, dismantled the mechanisms that would have absorbed the shock. What followed was not bad luck meeting a fragile economy. It was a predetermined arithmetic arriving on schedule.

On 12 June, 1,500 students marched on Jakarta’s Hotel Indonesia roundabout under a banner reading “Heading to Bankrupt Indonesia.” Two days earlier, Pertamina had raised Pertamax fuel prices 32%. The students were late to a conclusion the bond market had already reached.

Three Decisions Removed the Buffers Before the Storm Hit

Indonesia’s oil exposure is direct and quantifiable. The country sources approximately 19% of its crude imports through the Strait of Hormuz. Every USD 1 above the 2026 budget assumption of USD 70 per barrel adds IDR 10.3 trillion in subsidy costs. It returns only IDR 3.6 trillion in revenue. At sustained USD 100 oil, the annual shortfall exceeds IDR 300 trillion.

A solvent government with functioning FX mechanisms absorbs that. Indonesia no longer had either.

The first decision was Danantara. Earlier in 2026, President Prabowo Subianto directed commodity exports – Indonesia’s primary automatic foreign exchange stabiliser – into a sovereign wealth fund reporting directly to the presidency. The structure bypassed Bank Indonesia and market-rate pricing.

Kieran Curtis, Head of Emerging Markets Local Debt at Aberdeen in London, said the restructured arrangement was simply “not as efficient as exports finding their own market.” When the rupiah needed dollar inflows, the channel that had historically delivered them was no longer open.

The second was Bank Indonesia’s independence. Parliament passed legislation adding employment and growth objectives to the central bank’s mandate and extending parliamentary powers over monetary policy. Prabowo had also nominated his nephew as deputy governor. Foreign investors had priced BI’s autonomy as the structural anchor for Indonesian fixed income. That anchor was loosening before oil moved.

The third was fiscal headroom. The free meals programme – IDR 268 trillion (USD 15 billion) per year, 14% of the entire 2024 budget – was funded not by new revenues but by cuts to infrastructure and development spending. The absorptive capacity a shock required was gone before the shock arrived.

When Hormuz closed, all three failures activated at once. A falling rupiah raises the IDR cost of dollar-denominated obligations, which widens the fiscal deficit, which drives CDS spreads higher, which triggers capital outflows, which weakens the currency further. The oil price was the trigger. The policy sequencing was the cause.

The Currency Is Not Falling. It Is Feeding on Itself.

The rupiah is down 8% year-to-date and 7% from when the Iran conflict began, with the steepest three-week decline since 2020. Foreign holdings of Indonesian government bonds have collapsed from near 40% before the pandemic to 12.6% – a near 20-year low. Net foreign equity outflows reached USD 3.2 billion through end-May, the heaviest since 2009. Bank Indonesia delivered a 50-basis-point emergency rate hike in May and deployed USD 12 billion in reserves. Neither arrested the slide.

John Woods, Asia Chief Investment Officer at Lombard Odier, was unambiguous: “It is true, there is a doom-loop forming.” Persistent outflows at multi-year lows in bond and equity holdings, he noted, would continue to pressure the rupiah, liquidity and asset prices.

Tan Altundag, Investment Manager for Emerging Equities at Pictet Asset Management – which has reduced its Indonesian equity holdings – was equally direct: “Indonesia is suffering from a genuine confidence crisis.” The currency’s trajectory, he added, risks pushing up inflation, tightening financial conditions and compressing growth in sequence.

A currency under this momentum does not stabilise through central bank signalling. It stabilises when the policies that destroyed confidence are reversed. That has not happened.

A Downgrade Is Not the Same Event for Every Investor

Moody’s and Fitch have cut their Indonesian debt outlooks to negative, citing deteriorating policymaking credibility. S&P has conditioned its rating on fiscal consolidation – a condition the free meals programme and subsidy overhang make structurally difficult to meet. MSCI is reviewing Indonesian equity market standards; a demotion to frontier status remains a tail risk.

The transmission differs by position type.

Government bond holders face the most immediate trigger. A formal downgrade below investment grade activates mandatory liquidation from IG-mandate funds. Foreign ownership stands at 12.6% – a near 20-year low – leaving thin technical support for prices. Forced sellers in a thin market push yields higher, raise borrowing costs and add fiscal pressure at the moment the deficit is already under strain.

The IDX, down 42%, faces a second wave if a credit event triggers EM-mandate exclusions on top of the confidence-driven selling already in progress. The existing decline prices some of that risk. Not all of it.

Private credit and PE positions face a structurally separate problem. Covenant packages written in 2023 and 2024 – when IDR 16,000 was a conservative stress – now operate with the rupiah past IDR 18,000 and no reversal catalyst in view. IDR/USD mismatches that appeared manageable at underwriting are live breaches today. Exit proceeds in USD compress at every point above IDR 16,000, independently of operating performance.

Hemant Mishr, Chief Investment Officer at S CUBE Capital, named the repricing directly: Indonesia is no longer priced as a reliably orthodox emerging market, but as one carrying rising policy risk. The downgrade triggers by position type are mapped in the companion piece: What an Indonesian Downgrade Actually Does to Your Portfolio.

The Exit Requires Undoing What Was Done

The rupiah can stabilise. Indonesia’s resource endowment is intact. A credible reversal on Danantara’s structure, Bank Indonesia’s mandate and the fiscal trajectory would shift the confidence calculus. The conditions are not complex. They are three decisions Prabowo would have to publicly unmake – each central to his mandate, each publicly defended.

Mark Ledger-Evans, Asia-focused Emerging Markets Fixed Income Portfolio Manager at Ninety One, framed it without softening: “It is possible for countries to pull themselves out of a negative spiral where they have put themselves in that position to begin with.”

Possible. Not automatic. The managers pricing stabilisation as remote are not pessimists. They are reading the same political constraints the CDS market priced months ago.

References:

- Prabowo’s Populist Policies Propel a ‘Doom-Loop’ in Indonesian Markets – Jakarta Post / Reuters

- Indonesia Hikes Fuel Price 32% amid Inflation Fears – Gurutrade / Reuters

- Indonesian Students Protest Government Policies as Economic Pressures Grow – Associated Press

- Indonesian Students Protest Govt Policies amid Economic Strain – Al Jazeera

- The Hormuz Crisis and Indonesia’s Fiscal Position – Jakarta Post

{kind=link}