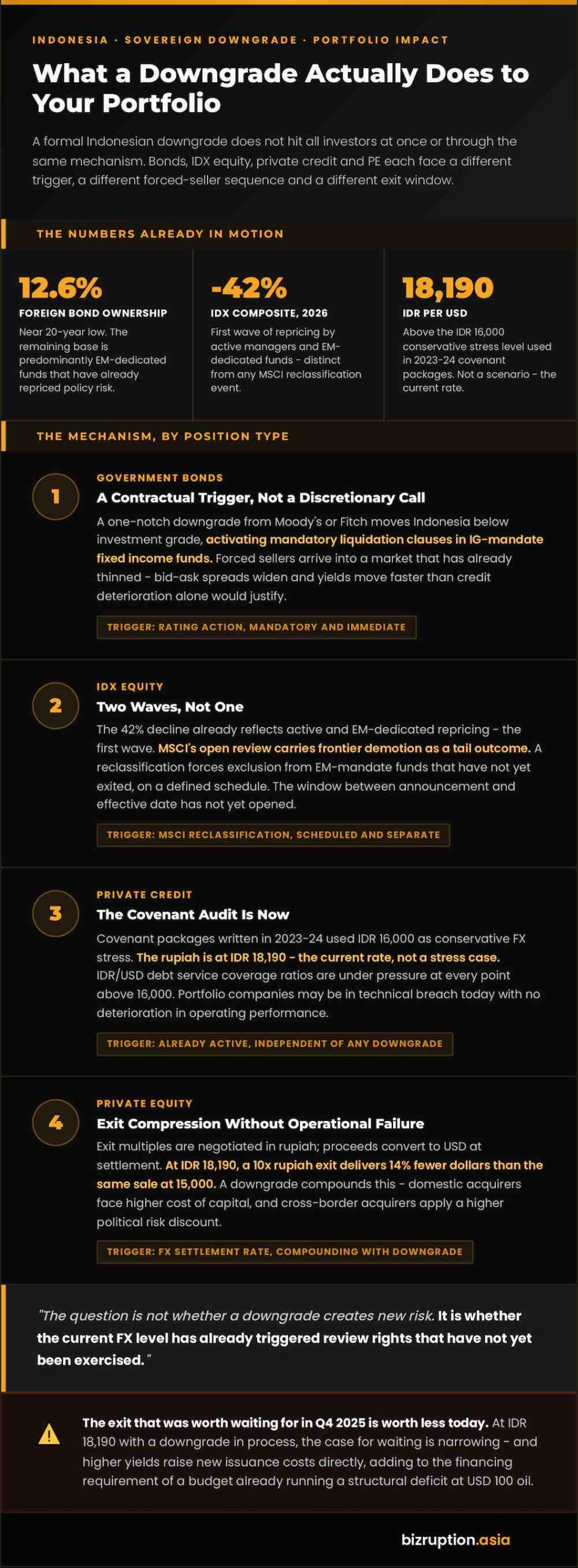

Moody’s and Fitch have both cut Indonesian sovereign debt outlooks to negative. A one-notch downgrade from either moves Indonesia below investment grade and activates mandatory liquidation clauses in IG-mandate fixed income funds. That is a contractual obligation, not a discretionary call.

Foreign ownership of Indonesian government bonds stands at 12.6%, a near 20-year low. The remaining base is predominantly EM-dedicated funds that have already repriced the policy risk. Forced sellers arriving after a formal downgrade sell into a market that has already thinned. Bid-ask spreads widen. Yields move faster than the credit deterioration alone would justify.

The secondary effect is fiscal. Higher yields raise new issuance costs directly. Each basis point increase adds to the financing requirement of a budget already running a structural deficit at USD 100 oil.

The three policy decisions that removed Indonesia’s buffers before the Hormuz shock arrived – and what they mean for the macro position – are in the cover story: The Shock Did Not Break Indonesia. The Decisions Made Before It Did.

IDX Equity: Two Waves, Not One

The Jakarta Composite is already down 42% in 2026, reflecting active managers and EM-dedicated funds repricing policy risk. That is the first wave. The second is structurally distinct.

MSCI’s open review of Indonesian equity market standards carries frontier demotion as a tail outcome. EM-mandate equity funds cannot hold frontier-classified securities. A reclassification forces exclusion from mandates that have not already exited – a technically separate forced-seller event arriving on a defined schedule.

The window between an MSCI announcement and its effective date is when the second wave can be positioned for. That window has not yet opened.

Private Credit: The Covenant Audit Is Now

For private credit managers, the downgrade scenario is secondary to a problem already active. Covenant packages written in 2023 and 2024 used IDR 16,000 as conservative FX stress. The rupiah is at IDR 18,190. That is not a stress scenario. It is the current rate.

IDR/USD financial maintenance covenants – debt service coverage ratios calculated in USD on IDR-denominated revenue – are under pressure at every point above IDR 16,000. Portfolio companies may be in technical breach today without any deterioration in operating performance. The question is not whether a downgrade creates new risk. It is whether the current FX level has already triggered review rights that have not yet been exercised.

PE: Exit Compression Without Operational Failure

Exit multiples are negotiated in rupiah. Proceeds convert to USD at the settlement rate. At IDR 18,190, a 10x rupiah exit delivers 14% fewer dollars than the same sale at IDR 15,000. Operating performance is irrelevant to that loss.

A formal downgrade compounds this through two channels. Domestic acquirers face higher cost of capital as Indonesian yields rise, narrowing the buyer pool. Cross-border acquirers apply a higher political risk discount, compressing the price they will pay.

The exit that was worth waiting for in Q4 2025 is worth less today. At IDR 18,190 with a downgrade in process, the case for waiting is narrowing.

{kind=link}