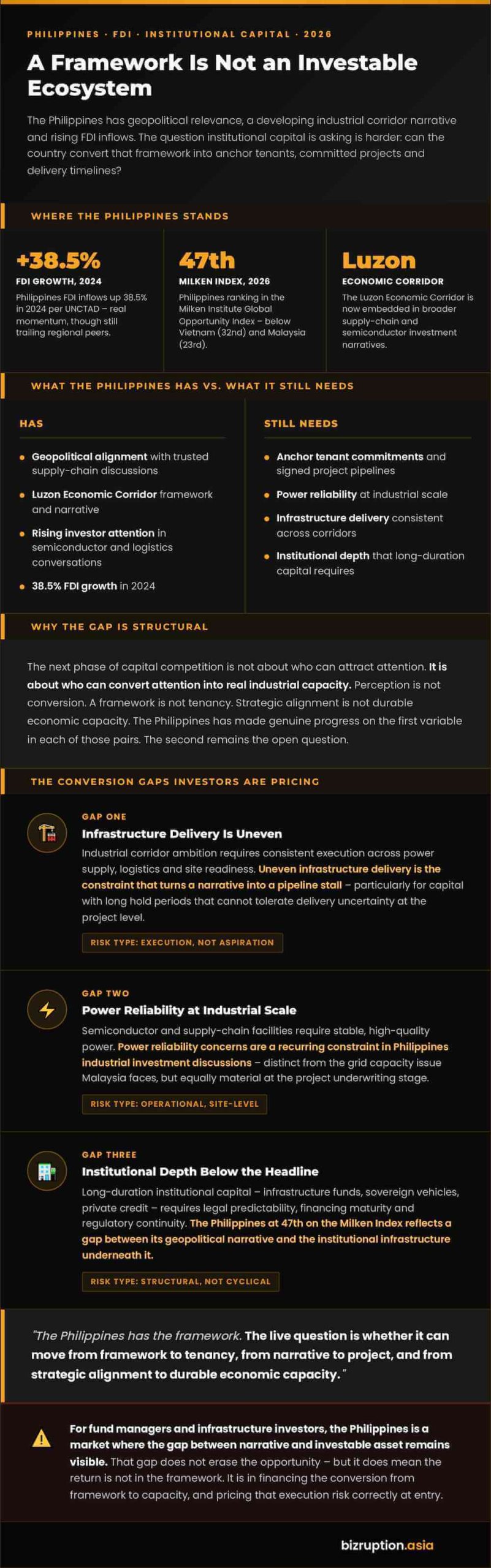

The Philippines is no longer being discussed only through remittances and consumption. It is appearing more often in supply-chain, semiconductor and industrial corridor discussions as investors look for alternatives across Asia.

That does not mean the investment case is solved.

The country’s framework has improved. The Luzon Economic Corridor has become part of the broader investment narrative, and the Philippines is being treated more seriously in discussions about trusted supply chains, logistics links and production capacity. But a framework is not the same as an investable ecosystem.

For institutional capital, the key question is not whether the Philippines has a story. It does. The question is whether it can convert that story into tenant commitments, operational infrastructure and the execution depth that long-duration investors require.

That is where the gap remains visible.

The Philippines still faces the familiar constraints that slow capital conversion: uneven infrastructure delivery, power reliability concerns, financing limitations and institutional bottlenecks. Those issues do not erase the opportunity, but they do make the shift from narrative to investable asset harder to achieve.

That matters because the next phase of capital competition is not about who can attract attention. It is about who can convert attention into real industrial capacity.

If Malaysia’s challenge is whether its digital buildout can stay ahead of grid pressure, the Philippines’ challenge is whether its geopolitical relevance can translate into physical and financial commitment. In both cases, the investment story is no longer about aspiration alone. It is about delivery.

The Philippines has made real progress in how it is perceived by global investors. It is being treated less as a remittance-consumption market and more as a potential production node in a broader Asian supply-chain map.

But perception is not the same as conversion.

The live question for fund managers, infrastructure investors and private equity principals is whether the Philippines can move from framework to tenancy, from narrative to project, and from strategic alignment to durable economic capacity.

That is the gap the market is now pricing or failing to price.

{kind=link}