OECD companies pledged US$ 55 billion for new ASEAN factories in 2022-2023; more than double the US$ 21 billion committed to China in the same period.

The China plus one supply chain strategy that boardrooms spent three years debating had, by 2024, produced a verified outcome: manufacturing FDI into ASEAN hit US$ 44 billion, greenfield investment in electronics and electrical equipment rose 15% to US$ 31 billion, and ASEAN held the top FDI position among developing economies for the fourth consecutive year.

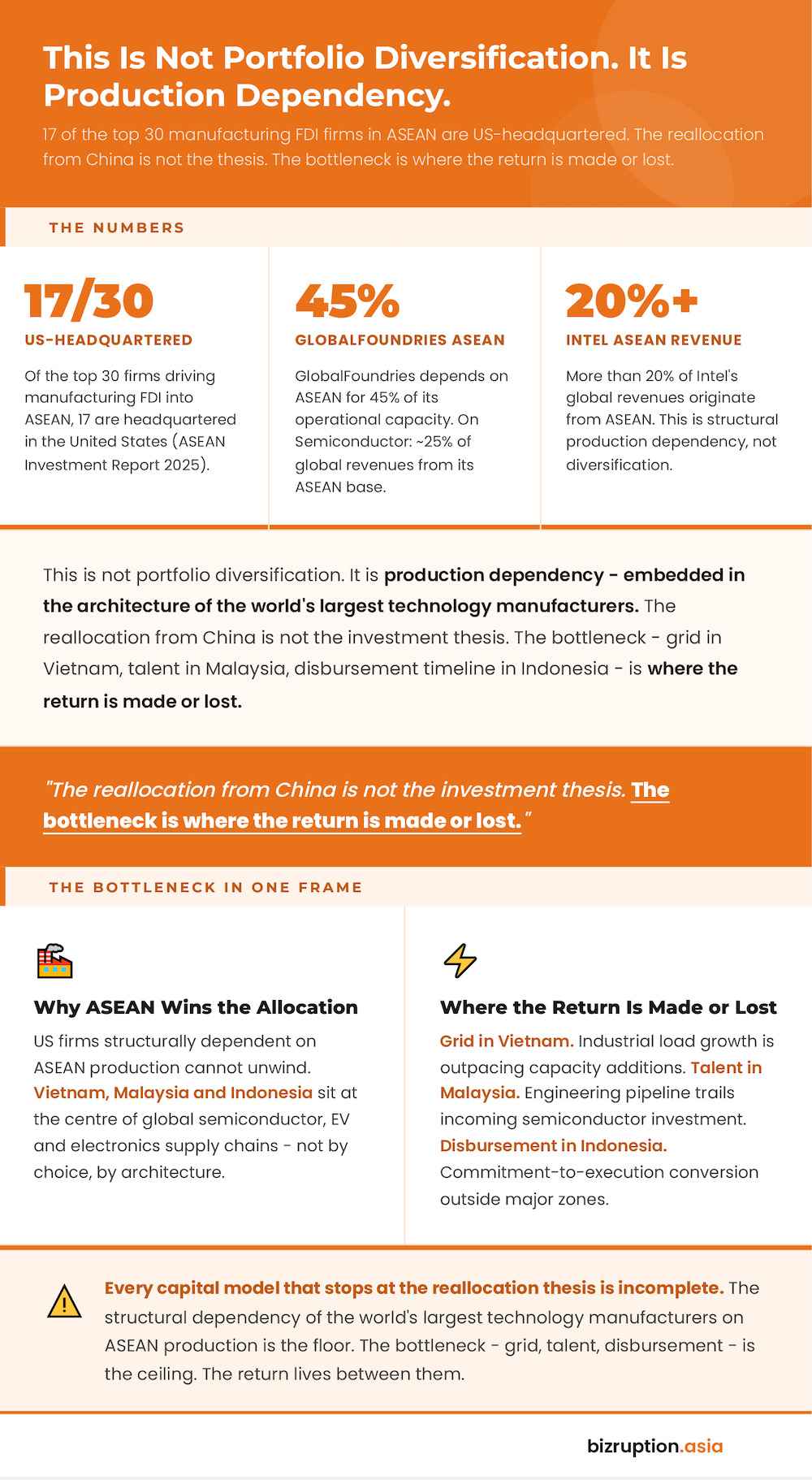

The reallocation is not a diversification exercise. Intel, Samsung, Global Foundries and On Semiconductor have built it into their production architecture. More than 20% of Intel’s global revenues trace back to ASEAN. These are operational dependencies, not portfolio positions.

The ASEAN Investment Report 2025 confirmed the scale, and delivered a judgment the investment promotion materials omitted: “Policy gaps, uneven implementation, skills shortages and infrastructure bottlenecks continue to limit the region’s ability to fully capture supply chain opportunities.”

The gap between capital arrived and infrastructure required to deploy it productively is equally structural. It differs in each market absorbing the bulk of the flow. and it belongs in every underwriting model before the next commitment is made.

Vietnam Manufacturing FDI: The Volume Leader Approaching Its Physical Ceiling

Vietnam posted the region’s strongest manufacturing FDI performance in 2025. Disbursed FDI reached US$ 27.6 billion – the highest in five years – with manufacturing and processing absorbing US$ 18.6 billion, or 59.2% of total registered capital, per Vietnam’s General Statistics Office.

GDP grew 8.02%. The numbers are not accidental. Intel, Samsung, LG and Foxconn all run material operations in the country.

Then Prime Minister Pham Minh Chinh formalised Vietnam’s semiconductor ambitions in Decision No. 1018/QD-TTg, signed September 2024: a roadmap targeting 100 chip design enterprises, a fabrication facility and 10 packaging and testing factories by 2030, with 50,000 engineers to staff them.

The binding constraint is not capital. It is electrons. Power demand for data centres and advanced manufacturing across the six largest ASEAN economies will quadruple from 2.6 GW to 10.7 GW between 2025 and 2035, per Ember Energy analysis cited in the ASEAN Investment Report 2025.

Vietnam’s industrial load is outpacing grid investment. For a PE principal underwriting a Vietnamese manufacturing asset on a five to seven-year hold, grid capacity is not a background risk. It is the underwriting question. The factories are arriving. The power to run them at scale is not.

Malaysia Semiconductor Investment: The High-Value Position with a Talent Pipeline Problem

Malaysia is not competing for Vietnam’s capital. The National Semiconductor Strategy, launched mid-2024, committed MYR 25 billion (US$ 5.3 billion) to front-end fabrication and local vendor development. Malaysia anchors the high-value end of ASEAN’s semiconductor supply chain.

Global Foundries relies on Malaysian facilities for 45% of its capacity at full production. On Semiconductor derives approximately 25% of global revenues from its ASEAN base. These are structural dependencies that place Malaysia’s investment environment in the same risk category as sovereign exposure for the companies carrying them.

The workforce is the constraint. Malaysia’s smaller labour pool and higher wages price it out of volume-oriented manufacturing flowing to Vietnam and Indonesia. The National Semiconductor Strategy targets segments – advanced packaging, front-end fabrication, medical devices – where engineering depth beats headcount.

That is the correct call. The risk is pace. Universities and technical institutions are not producing engineers at the speed the incoming investment requires. Announced capacity and operational capacity are diverging.

For investors pricing Malaysian manufacturing exposure, the talent delivery timeline is where the deal thesis meets its test.

Indonesia FDI: The Scale Argument Carrying an Execution Premium

No other ASEAN market enters the manufacturing reallocation with Indonesia’s combination: 280 million consumers, silica sand reserves anchoring downstream semiconductor input processing, and a national semiconductor roadmap targeting production localisation.

Infineon committed to backend fabrication. Nvidia anchored AI data centre investment. Both bets share the same logic – Indonesia’s resource base and domestic market scale create a manufacturing rationale export competitiveness alone cannot replicate.

The pricing variable is execution. Indonesia ranks consistently among ASEAN’s top FDI announcement destinations and converts those announcements into disbursed, operational capital more slowly than either Vietnam or Malaysia.

The causes are specific: land acquisition timelines, licencing complexity outside major industrial zones, infrastructure gaps beyond Java, and friction between central and regional approval processes.

Kearney’s 2026 FDI Confidence Index, drawing on 507 senior executives, found 84% of global investors rate industrial policy as extremely or very important to investment decisions.

Indonesia’s policy settings are competitive. Its implementation architecture carries a risk premium Vietnam and Malaysia do not – not a reason to exit the allocation, but a reason to price the timeline correctly.

Three Bottlenecks, Three Underwriting Models

Bain’s Asia-Pacific Private Equity Report 2026 recorded APAC PE deal multiples at 13.4 times EBITDA in 2025. At that price, earnings predictability is not a preference. It is a requirement. Vietnam delivers volume and a five-year disbursement track record against a grid ceiling that capital can solve on a defined timeline.

Malaysia delivers value chain position and regulatory consistency. Its ceiling is a talent pipeline that workforce development cannot accelerate on demand. Indonesia delivers scale and resource depth against an execution ceiling that demands a higher IRR hurdle and a longer hold.

Fund managers and PE principals building ASEAN manufacturing exposure are not making one regional call. They are making three separate underwriting decisions – each with a distinct bottleneck, a distinct exit profile and a distinct return threshold. Price them as one thesis and at least two are wrong.

References:

- ASEAN Investment Report 2025: Foreign Direct Investment and Supply Chain Development – ASEAN Secretariat and UNCTAD

- Vietnam’s Economy in 2025: GDP, FDI and Trade – Vietnam Briefing

- Vietnam FDI H1 2025: Highest Figure in Five Years – Site Location Adviser

- Vietnam Q1 2026 FDI Data – Trading Economics / General Statistics Office of Vietnam

- Vietnam’s Bold Semiconductor Gambit – Financial Content / Financial News

- AI and Compute Infrastructure: Building ASEAN’s Digital Backbone – ASEAN Exchanges

- The ASEAN Semiconductor Ascent: From Assembly Lines to Advanced Innovation – SlideShare / Industry Analysis

- Regional Competition for FDI: How Vietnam Stacks Up Against Indonesia, Thailand and Malaysia – D’Andrea and Partners

- Kearney’s 2026 FDI Confidence Index Finds Investors Recalibrating Strategies – Kearney

- Asia-Pacific Private Equity Report 2026 – Bain and Company

{kind=link}