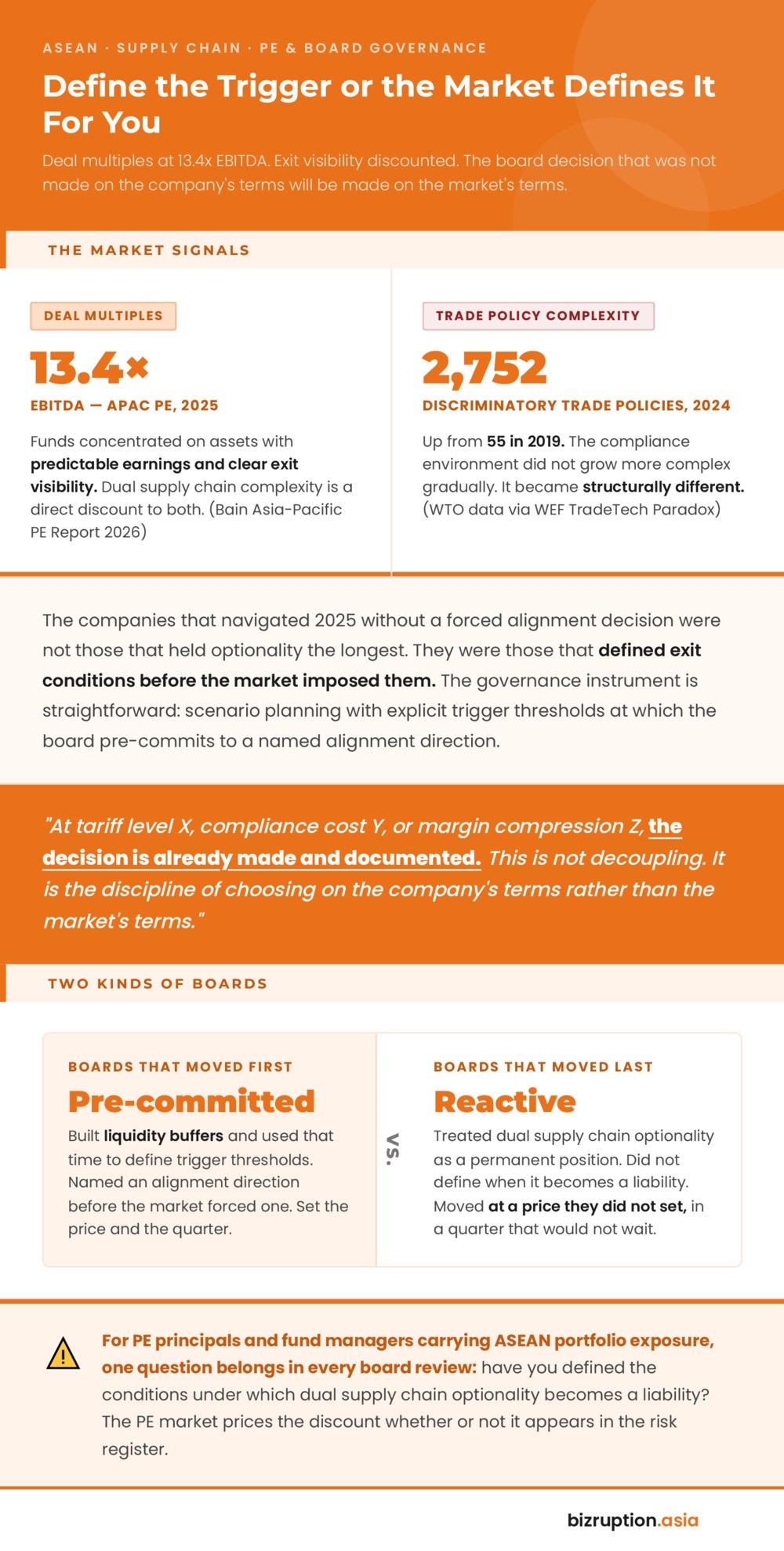

The WTO counted 55 discriminatory trade policies in 2019. By 2024, that number was 2,752 – documented in the WEF’s TradeTech Paradox report published in January 2026. Each policy is a rule set. For Southeast Asian companies operating across both the US-aligned and Chinese-aligned corridors from a single base, each new rule set lands on both sides of the ledger at once.

The cost does not spread. It compounds.

McKinsey Global Institute’s March 2026 analysis of global trade geometry confirms that US-China bilateral trade fell approximately 30% as tariffs tightened in 2025, while ASEAN grew exports to both economies at the same time. No other major economic bloc achieved this.

That is the number in the trade headlines. What does not appear is what sustaining that position costs at the operating company level – and at what point the hidden compliance burden exceeds the margin it was built to protect.

The Gap Between the Trade Data and the Operating Reality

Deloitte’s 2025 Asia Pacific Tax and Tariff Complexity Survey of 363 senior regional executives found that nearly 70% have shifted their primary supply chain focus from cost minimisation to reliability, stability or strategic alignment.

Eunice Kuo, Deloitte Asia Pacific Tax and Legal Leader, told companies to “treat cost signals as early warnings, align ecosystems beyond cost, and embed digital enablement at the core.”

What the survey did not measure is how many of those 70% have modelled the full cost of maintaining dual supply chain alignment at the company level. Judged by board behaviour across Southeast Asia, the answer is not many.

The dual-corridor strategy was designed for a world in which the two systems diverged slowly enough to manage. That world ended somewhere between 2019 and 2024.

A company that could absorb 55 discriminatory policies does not carry the same cost structure at 2,752. That is not a rounding error. It is a structural shift in what dual supply chain exposure costs per operating year.

Where the Compliance Cost Has Become Incompatibility

Three sectors have crossed from elevated compliance cost into hard structural incompatibility.

In electronics and semiconductor assembly, ITAR restrictions and Chinese export control countermeasures now target overlapping product categories. A component cleared for US defence-adjacent supply chains cannot, under a growing list of classifications, ship to Chinese state-linked customers.

Apple is the clearest public benchmark: more than USD 1 billion invested in Indian manufacturing since 2023 to reduce China exposure, with a 10% increase in lead times on some product lines as the direct operational consequence.

In financial services, banks running correspondent relationships across both SWIFT and CIPS rails absorb compliance infrastructure costs that compress net interest margin on cross-border books before they surface in any risk disclosure. The cost appears in every quarter’s operating expense line.

It is invisible to a fund manager reading a standard filing.

In technology infrastructure, US cloud security certification and China’s data localisation obligations under the Personal Information Protection Law rest on incompatible architectural assumptions. Serving enterprise customers across both corridors from a single technology stack is no longer a legal grey area.

It requires duplicate infrastructure – a capital cost sitting unattributed on the balance sheet of every company that has not yet made an alignment decision.

Why Boards Are Not Acting and Why That Window Is Closing

McKinsey’s December 2025 CFO Pulse Survey of 152 global finance leaders found that 37% name geopolitical instability as their company’s greatest growth risk. The dominant response: 60% are building liquidity buffers. Only one in three expressed confidence in their organisation’s ability to manage trade policy change.

A buffer buys time. It does not shrink the compliance cost accumulating beneath it, and it does not resolve the incompatibility taking hold in the three sectors above.

The policy environment is hardening around that delay. Kearney’s 2026 FDI Confidence Index, drawing on 507 senior executives surveyed in January 2026, found that 84% of global investors rate industrial policy as extremely or very important to their investment decisions.

Shigeru Sekinada, Region Chair, Asia Pacific at Kearney, said “the APAC region emerges as a winner as investors recalibrate how they make decisions in a more turbulent operating environment.”

Recalibration, in practice, means the policy architecture determining corridor alignment is tightening on both sides at once. The window for deferring the alignment decision is narrowing from both directions.

What Acting Before the Window Closes Looks Like

Bain’s Asia-Pacific Private Equity Report 2026 recorded deal multiples at 13.4 times EBITDA in 2025, with funds concentrating capital on assets carrying predictable earnings and clear exit visibility. Unresolved dual supply chain complexity at board level is a direct discount to exit visibility.

PE funds price it into valuations whether or not the target company names it in a risk register. The discount is already in the market. The question is whether it is in the board’s analysis.

The companies that navigated 2025 without a forced alignment decision were not those that held optionality the longest. They were those that defined exit conditions before the market imposed them.

The governance instrument is straightforward: scenario planning with explicit trigger thresholds at which the board pre-commits to a named alignment direction.

At tariff level X, compliance cost Y, or margin compression Z, the decision is already made and documented. This is not decoupling. It is the discipline of choosing on the company’s terms rather than the market’s terms.

For PE principals and fund managers carrying ASEAN portfolio exposure, one question belongs in every board review: have you defined the conditions under which dual supply chain optionality becomes a liability?

The CFOs who built liquidity buffers bought time. The boards that used that time to answer the question will move first. The rest will move last – at a price they did not set, in a quarter that will not wait.

References:

- Geopolitics and the Geometry of Global Trade: 2026 Update – McKinsey Global Institute

- The TradeTech Paradox: Connectivity Amid Fragmentation – World Economic Forum

- Cost Increases of 21-40% Trigger Supply Chain Overhauls for Nearly Half of APAC Businesses – Deloitte Asia Pacific

- How CFOs Build Resilience Against Geopolitical Uncertainty – McKinsey

- Kearney’s 2026 FDI Confidence Index Finds Investors Recalibrating Strategies Amid Geopolitical Tension and Industrial Policy Expansion – Kearney

- Asia-Pacific Private Equity Report 2026 – Bain and Company

- Global Risks Report 2026 – World Economic Forum

{kind=link}