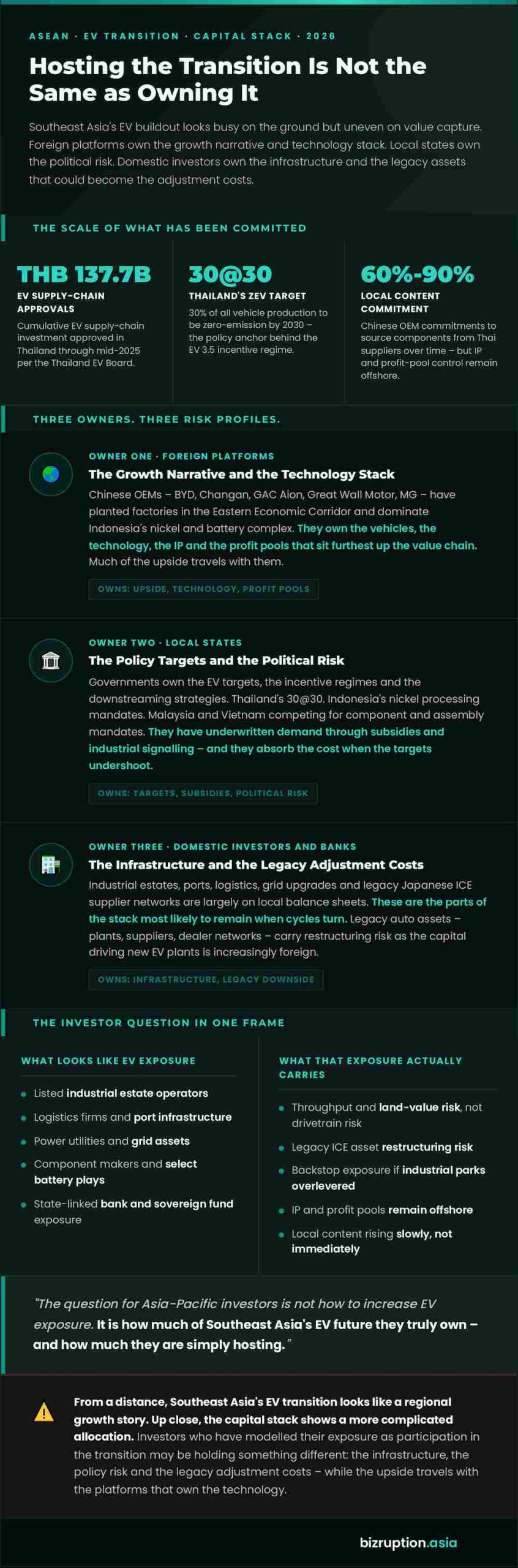

Thailand’s EV buildout is a case in point. Chinese brands including BYD, Changan, GAC Aion, Great Wall Motor and MG have planted factories in the Eastern Economic Corridor, backed by incentives that helped push cumulative EV supplychain approvals past 137.7 billion Baht by mid2025.

Indonesia’s nickel and battery complex, Vietnam’s EV assembly ambitions and Malaysia’s component and semiconductor base round out a region that looks busy on the ground but uneven on value capture.

This piece looks at who actually owns Southeast Asia’s EV transition, and what that means for investors deciding how much of this story they really hold.

Chinese Platforms Own the Growth Narrative. Local States Own the Targets

Across ASEAN, Chinese EV manufacturers and suppliers have emerged as the most aggressive capital providers in frontend vehicle production and key components. In Thailand, Chinese investment in EV projects in the Eastern Economic Corridor has outpaced other foreign sources, with BYD and peers using the country as both a domestic base and export hub.

In Indonesia, Chineselinked consortia dominate the nickel and battery projects that underpin EV supply chains, often under longterm offtake and processing arrangements.

Governments, meanwhile, own the policy targets and political risk. Thailand’s 30@30 ambition – 30% of production as zeroemission vehicles by 2030 – anchors its EV 3.5 regime. Indonesia’s downstreaming strategy hinges on keeping more value from nickel and batteries onshore. Vietnam and Malaysia are competing for assembly, electronics and component mandates.

For investors, this split matters: foreign platforms own much of the growth narrative and technology stack, while local states have underwritten demand through subsidies, targets and industrialpolicy signalling.

Local Capital Is Heaviest in Infrastructure and Legacy Assets

Domestic investors and banks are most heavily exposed in two areas: infrastructure and legacy automotive assets. Industrial estates, ports, logistics and grid upgrades across Thailand’s Eastern Economic Corridor, Indonesia’s industrial parks and Malaysia’s manufacturing corridors are often financed with a mix of statelinked capital, local banks and domestic REIT or infrastructure vehicles.

These assets are platformagnostic – they carry throughput and landvalue risk rather than drivetrain risk – but they are also the parts of the stack most likely to remain on local balance sheets when cycles turn.

At the same time, legacy auto assets in Thailand, Indonesia and Malaysia – plants, suppliers and dealer networks built around Japanese ICE platforms – are still largely held by domestic investors, banks and, in some cases, regional private equity.

As EV adoption rises unevenly and foreign platforms expand, these legacy assets carry the downside risk of underutilisation, restructuring and writedowns. The capital that financed them is local; the capital driving the new EV plants is increasingly foreign.

Public Markets and Sovereign Capital Hold a Thin Sliver of the Upside

For publicmarket and sovereign investors, the direct equity slice of Southeast Asia’s EV transition is thinner than the headlines suggest. Listed beneficiaries include industrial estate operators, logistics firms, power utilities, component makers and a handful of vehicle and battery plays, but many of the most powerful profit pools sit in privately held foreign OEMs and their offshore supply chains.

Even where Chinese manufacturers commit to higher local content – sourcing 60% – 90% of components from Thai suppliers over time, for example – the intellectual property and profitpool control often remain offshore.

Sovereign funds and longonly institutional investors can gain exposure through these listed proxies and through selective private deals in infrastructure, batteries and components.

But they also remain backstops: as lenders or shareholders of statelinked banks and utilities, they ultimately bear part of the risk if legacy auto assets or overlevered industrial parks struggle through the transition.

The Investor Question: How Much of the Transition Do You Really Own?

From a distance, Southeast Asia’s EV transition looks like a regional growth story. Up close, the capital stack shows a more complicated allocation: foreign platforms own much of the upside in vehicles and technology; local states own the political risk; domestic banks and investors own the infrastructure and many of the legacy assets that could turn into adjustment costs.

For AsiaPacific investors, the practical question is not just how to increase “EV exposure” in portfolios. It is how much of Southeast Asia’s EV future they truly own, and how much of it they are simply hosting.

References:

- EV Market in ASEAN: Policies, Current Status & Framework – rieti.go

- Chinese investment fuels Thailand’s ambition as global export hub – chinadaily.com

- BOI records THB 137.7 billion in approved investments for Thailand’s emobility supply chain – marklines

- EV 3.5 package: Board of Investment of Thailand – boi.go

- Government Supports EV 3.5 Measures to Promote the Use of Electric Vehicles – PRD

- Chinese carmakers rev up EV production in South-east Asia but net gains to local workers uncertain – straitstimes

- EV Market in ASEAN: Policies, Current Status & Framework – RIETI / Purwanto

- China’s EV Boom and Southeast Asia – indo-pacificstudiescenter

- Chinese EVs are putting a high-tech spin on “Made in …” – channelnewsasia

- Chinese EV makers win over Southeast Asians with cut-price deals – kr-asia

{kind=link}