Ten million Filipinos work abroad. Their transfers home – USD 37.2 billion in 2025 – funded Philippine household consumption for three decades, smoothed every current account deficit and allowed Manila to run a growth model it never had to replace.

That model is now under pressure from three directions simultaneously. The World Bank has put a number on what that means: 3.7% GDP growth in 2026, down from 5.3% projected in January, 1.3 percentage points below the government’s own floor target.

The gap is not a rounding error. It is the distance between an economy growing at its structural potential and one whose only reliable engine is misfiring for the first time in a generation.

Three Pressures on One Engine

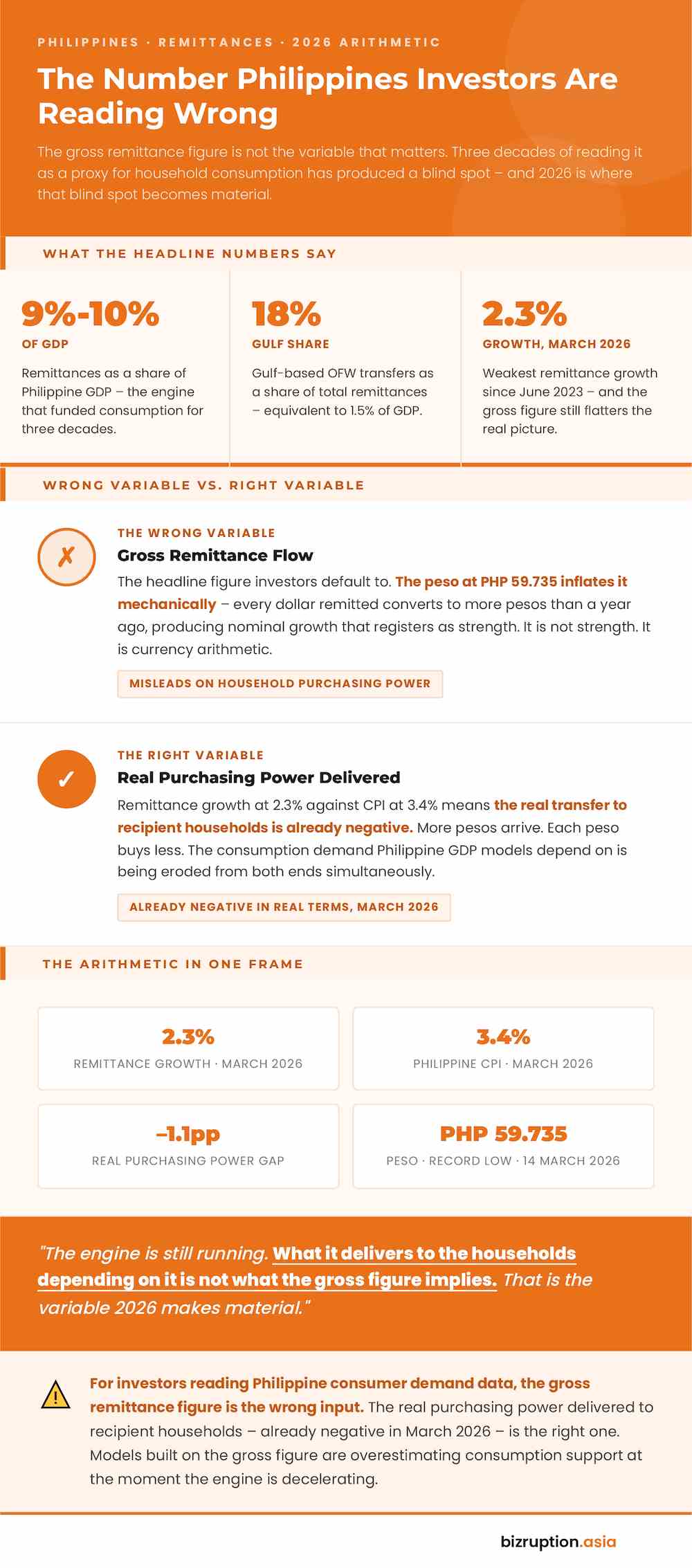

The first is geographically direct. The Middle East hosts 2.5 million Filipino workers whose transfers account for 18% of total OFW remittances – 1.5% of GDP, per MUFG Bank research published 9 March 2026. BSP Governor Eli Remolona acknowledged the exposure on CNBC, noting downside risk to Gulf labour demand. “We’re a top exporter of labor services,” he said.

Shilan Shan, deputy chief emerging markets economist at Capital Economics, was sharper: a Gulf remittance drop would widen external deficits “at a time when high energy prices will already be pushing deficits deeper.”

The second pressure is the peso. It closed at PHP 59.735 on 14 March 2026, a record low. Depreciation inflates the peso value of each dollar remitted – which is why March data showed nominal growth while household purchasing power fell.

Peso depreciation inflates the dollar value of each transfer on paper. But with Philippine CPI at 3.4% in March 2026 and remittance growth at 2.3%, the purchasing power those transfers deliver has shrunk. Recipient households are receiving more pesos that buy less.

The third is oil. Over 36% of the Philippine CPI basket is directly or indirectly exposed to energy prices, per National Statistician Claire Dennis Mapa. MUFG estimates every USD 10 per barrel increase cuts GDP growth by 0.2 percentage points and lifts inflation by 0.6 percentage points.

With Brent above USD 100 through mid-March and the World Bank’s full-year baseline at USD 94, the arithmetic hits the household on both fronts: remittances arrive worth less in real terms, and the cost of everything they buy is rising.

The BSP Is Caught Between Two Fires

The BSP entered 2026 in easing mode. MUFG’s base case as of 9 March projected two further rate cuts to 3.75% by October – contingent on oil falling toward USD 70 by Q2 2026. Oil is at USD 94 on the World Bank’s full-year baseline. It was above USD 100 through mid-March. The cycle the BSP planned is not the one it can deliver.

Remolona stated publicly that USD 100 oil (already exceeded) could force the BSP to end easing. MUFG models show sustained oil above USD 100 pushes Philippine inflation above the 4% upper target in 2026 and into 2027. A central bank hiking into 3.7% growth is not managing an oil shock. It is managing a stagflationary trap.

The external position tightens the corner further. MUFG estimates USD 100 oil widens the current account deficit to approximately 3% of GDP. A deficit at 3% of GDP pressures the peso directly. A weaker peso raises the PHP cost of oil imports. The loop runs without a new external trigger.

What the 2028 Number Actually Signals

The World Bank projects recovery to 5.6% in 2027 and 2028 – within the government’s target band. Two conditions underpin it: geopolitical uncertainty dissipating and energy prices stabilising. Both are assumptions, not forecasts.

The World Bank’s own downside scenario puts global output at 1.3% in 2026 under sustained energy disruption and financial market stress. The Philippines – ranked among ASEAN’s most oil-exposed economies by MUFG, with over 36% of its CPI basket tied to energy prices – sits in the upper range of that exposure.

Ser Percival Pena-Reyes, Senior Research Fellow at the Ateneo Center for Economic Research and Development, named the structural question the 3.7% figure raises. “The key question is whether the Philippines can lift its potential growth rate rather than simply recover cyclically,” he said.

Marco Agonia, economist at the University of Asia and the Pacific, identified the signal beneath the projection. “The traditional driver of the Filipino growth engine, remittance-led consumption, is petering out,” he said. A cyclical rebound in 2027 – driven by base effects and infrastructure spending – does not answer what permanently replaces it.

For fund managers with Philippine equity exposure, peso depreciation and BSP rate reversal risk are already in 2026 models. The question not yet priced is structural: if Gulf labour flows slow permanently, the 2027 recovery is not a return to form. It is a one-time reprieve before a reckoning the Philippines has not yet prepared for.

References:

- World Bank Global Economic Prospects, June 2026

- World Bank Sees Philippines Growing Just 3.7% in 2026 amid Middle East War – Manila Bulletin, 12 June 2026

- World Bank: Oil Relief May Strain Philippine Finances, Further Slow Growth – Manila Bulletin, 9 April 2026

- Philippines – Strait of Hormuz Closure: Impact of Higher Oil Prices and More – MUFG Research, Michael Wan, 9 March 2026

- Remittance Risks, Oil Shock Cloud Philippines Economic Outlook – Philstar, 9 March 2026

- Middle East Conflict May Hit OFW Remittances, Peso – Capital Economics, Manila Bulletin, 13 March 2026

- OFW Remittances Hit 9-Month Low in February: BSP – Tribune, 15 April 2026

- Despite Middle East War, PHL Remittances Up 2.3% – BusinessMirror, 16 May 2026

- OFW Remittances Rise, but Future Uncertain – BusinessMirror, 17 March 2026

{kind=link}