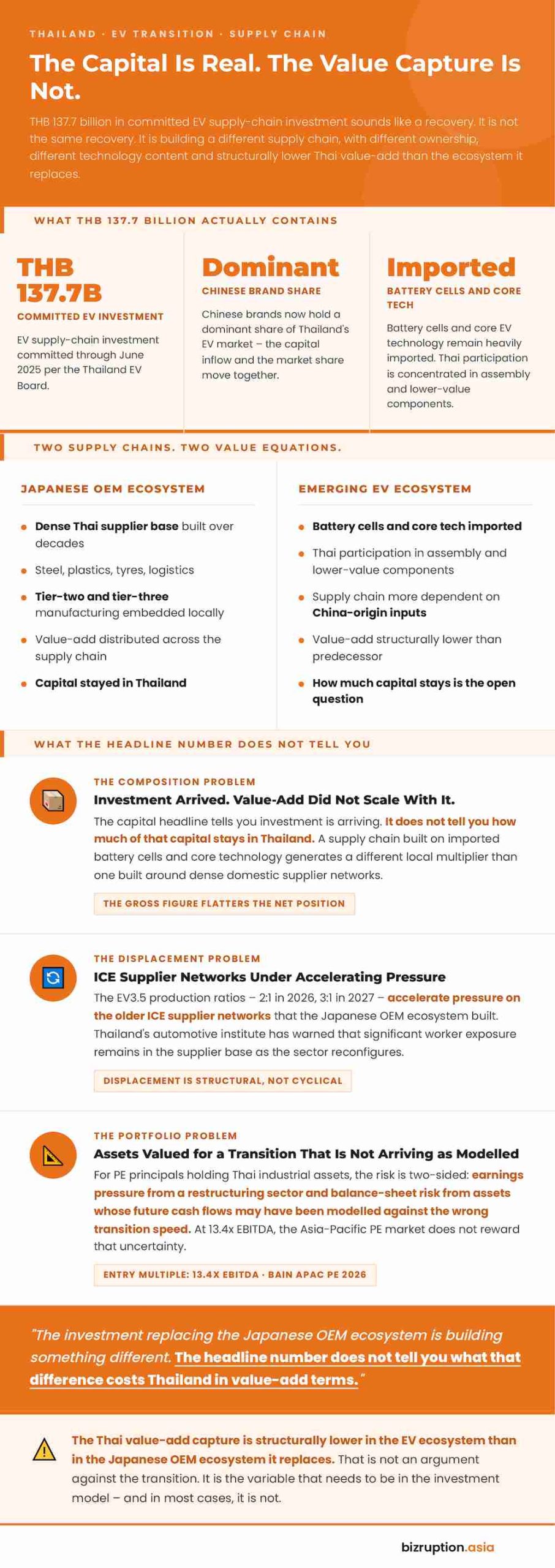

In April 2026, the Federation of Thai Industries reported that Thailand produced 369,751 vehicles in Q1 2026, up 5.3% year-on-year and the first quarterly increase in six quarters. The BOI has also confirmed 137.7 billion baht in committed EV supply-chain investment through June 2025. Both figures are real. Neither tells the story that fund managers and private equity principals with Thai automotive exposure actually need.

The Q1 recovery was partly driven by compensatory production requirements under Thailand’s EV incentive framework, not by a clean return to organic demand. The investment pipeline is building a supply chain with different ownership, different technology content and different value capture from the one it is replacing. That is the variable that does not appear in the headline numbers.

The Production Numbers Are Real. The Recovery Story Is Not

Thailand produced 1.47 million vehicles in 2024, down 26.5% from 2019. Domestic sales also fell sharply in 2024, marking one of the weakest periods for the sector in years. Honda has already closed its Ayutthaya vehicle assembly line, while Nissan, Suzuki and Subaru have consolidated or exited Thai production altogether.

That does not mean the sector is stabilised. BEV output in 2024 remained a small share of total production, and the spike in EV assembly late in 2025 reflected production-offset obligations rather than a clean demand-led rebound. Surapong Paisitpatanapong of the Federation of Thai Industries said the domestic production spike was tied to companies fulfilling those compensation requirements.

For investors reading the production figures, the context matters. A factory meeting a regulatory deadline is not the same as a factory running because end-demand has returned.

The EV Investment Is Replacing One Supply Chain with Another

The 137.7 billion baht in committed EV supply-chain investment is real capital, but the more important question is what it is building and who captures the value. Japan’s OEM ecosystem spent decades building a dense Thai supplier base across steel, plastics, tyres, logistics and tier-two and tier-three manufacturing.

The emerging EV ecosystem is different. Chinese brands now dominate Thailand’s EV market and the supply chain is more dependent on imported battery cells and core technology, with Thai participation still concentrated in assembly and lower-value components.

That matters because the capital headline tells you investment is arriving. It does not tell you how much of that capital stays in Thailand.

The EV3.5 framework also raises the domestic production ratio to 2:1 in 2026 and 3:1 in 2027 for imported EVs under the scheme, while the government continues to support a broader electrification transition.

That creates a more structured path for production commitments, but it also accelerates the pressure on older ICE supplier networks. Thailand’s automotive institute has warned that a large number of workers remain exposed to displacement as the sector reconfigures.

For private equity principals holding Thai industrial assets, that creates two forms of risk at once: earnings pressure from a restructuring sector and balance-sheet risk from assets whose future cash flows may have been modelled against the wrong transition speed.

The Japanese Signal the Market Has Not Priced

Masato Otaka, Japan’s ambassador to Thailand, said at The Standard Economic Forum on 29 June 2026 that “EV is not a singular answer.” That line matters because it reflects a broader multi-pathway argument – EVs, hybrids and biofuels in parallel – that aligns with the commercial interests of Japanese OEMs still tied to existing Thai production.

Thailand’s 30@30 target remains a policy ambition rather than a fully binding industrial endpoint. If the government continues to lean toward a multi-pathway approach, the transition will stay slower and more uneven than a pure-EV narrative suggests.

That extends the window for Japanese OEM production. It also extends the uncertainty for suppliers caught between two industrial architectures with different technology paths and different capital needs.

The market is not yet pricing that tension cleanly.

The Portfolio Question the Headline Numbers Do Not Answer

At current valuations, the Asia-Pacific private equity market does not reward earnings uncertainty. The Thai automotive sector carries structural uncertainty on two axes: the speed of Chinese EV capital displacing Japanese supplier networks, and the extent to which Thailand’s policy path stays on a multi-track rather than a pure-EV trajectory.

The sector is not at a crossroads. It has already taken one turn. Production has fallen, Japanese capital has consolidated and Chinese EV capital has entered. The question for investors is whether the assets they hold were valued for the road already taken or the one they were told was coming.

References:

- Thailand Automotive Institute – Facts and Figures 2024

- FTI / MarkLines – Thailand Vehicle Production 2024 and 2025 Monthly Data

- FTI – Q1 2026 Production Report via MarkLines, 27 April 2026

- Thailand EV Board – EV Supply Chain Investment Tops 137.7 Billion Baht, 30 July 2025

- Thailand EV Board – Thailand’s National Electric Vehicle Policy Committee / EV Board

- Board of Investment of Thailand – EV 3.5 Policy and Investment Data

- Nation Thailand – Thai EV Production Skyrockets by 1,974% as Offset Deadlines Loom, 22 December 2025

- Bain and Company – Asia-Pacific Private Equity Report 2026

- The Standard Economic Forum – Thailand’s ‘Detroit of Asia’ Label at Crossroads, 29 June 2026

{kind=link}