ASEAN’s central banks did not send their finance ministers to Samarkand, Uzbekistan on 3 May 2026 to declare a crisis. They went to endorse directions, task deputies and issue a communiqué. What came out reads like a damage assessment. Growth moderating. Inflation rising. Capital flows volatile. Exchange rates under pressure.

The 29th ASEAN+3 Finance Ministers’ and Central Bank Governors’ Meeting (AFMGM) was not describing risks approaching the region – it was confirming conditions already present across eleven economies. All traceable to a single trigger: the Middle East conflict that shut the Strait of Hormuz and drove energy, fertiliser and freight costs through the regional economy in the same week.

What the statement did not say, but what its language makes unavoidable, is that the architecture underpinning those central banks – the regional safety net, the multilateral surveillance office, the green finance facilities now assembling – was engineered for a world in which crises arrive one at a time.

A Safety Net Built for a Single Channel

The Chiang Mai Initiative Multilateralisation (CMIM) was designed in the aftermath of the 1997-98 Asian Financial Crisis. Its logic was liquidity: member economies facing sudden balance of payments pressure could draw on a pooled USD 240 billion reserve facility, with conditionality linked to IMF programme alignment.

The ASEAN+3 Macroeconomic Research Office, established in 2011, provides the surveillance function that makes CMIM activation credible. Both institutions were built for crises that arrive through one dominant channel – currency pressure, capital flight, sovereign liquidity stress – and yield to a single policy lever.

The current shock does not work that way. The Samarkand statement maps the cascade: higher oil and gas prices tighten financial conditions, which accelerates capital flow volatility, which pressures exchange rates, which widens current account deficits, which strains subsidy budgets already at their limits.

Running in parallel: flash floods and extreme weather across the region in 2025 and early 2026 destroyed crops, forced emergency fiscal responses and compressed the policy space central banks need to manoeuvre. Bank balance sheets carrying agricultural and infrastructure loan books are absorbing credit stress from the energy and climate channels at the same time.

No regional stress-test framework was calibrated for that combination. The CMIM was not built to absorb it.

Aziz Durrani and Julia Anna Bingler, writing in The Business Times in October 2025, put the gap plainly: national initiatives to manage these risks “remain fragmented and often modest in scale relative to the magnitude of the risks ahead.” The toolkit is not failing. It is solving the right problem for the wrong crisis.

What Is Being Built and What It Cannot Yet Do

Recognising the mismatch, the Philippines’ 2026 ASEAN chairmanship has pushed sustainable finance onto the Finance Track agenda with two concrete instruments.

The ASEAN Catalytic Green Finance (ACGF) Facility – a USD 1.9 billion vehicle managed by ADB under the ASEAN Infrastructure Fund – confirmed a lending pipeline of USD 19.4 billion across 30 projects for 2026-2028, as cited in the joint statement of the 13th ASEAN Finance Ministers’ and Central Bank Governors’ Meeting, convened virtually from 7 to 10 April 2026.

The ACGF’s 2025 annual report recorded the facility’s strongest year since its 2019 launch: four project approvals in Cambodia, Indonesia and Lao PDR.

The Regional Connectivity Fund for Energy, launched under the ASEAN Infrastructure Fund on 7 April 2026, was welcomed at the same meeting as a step toward the ASEAN Power Grid. The ADB’s proposed USD 30 billion facility for 2026–2030 adds institutional weight behind the direction.

These are real instruments addressing a real gap. The constraint is sequencing. Technical assistance and de-risking precede financing approvals. Financing approvals precede disbursement. Disbursement precedes capital absorbing risk in the field. USD 19.4 billion identified for 2026-2028 is not USD 19.4 billion operational. The compound shock is not waiting.

The Fragmentation That Survives Even a Successful Build-Out

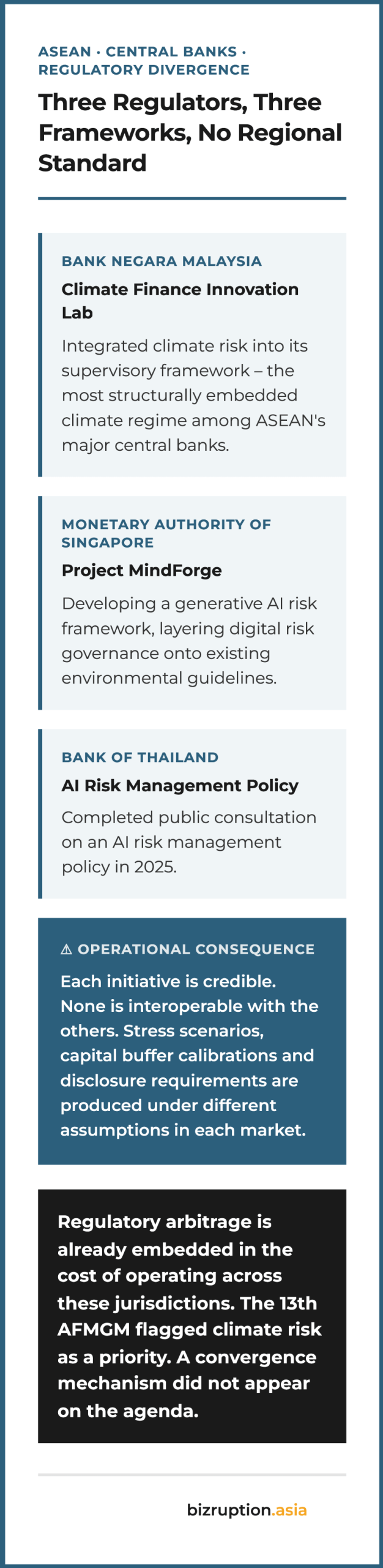

The pipeline problem has a structural companion that facility funding alone cannot resolve. Across ASEAN, the supervisors that govern how commercial banks and insurers price, provision and stress-test for compound risks are each running their own national framework. None of those frameworks speak to each other.

Bank Negara Malaysia launched a Climate Finance Innovation Lab and integrated climate risk into its supervisory model. The Monetary Authority of Singapore is developing a generative AI risk framework through Project MindForge. The Bank of Thailand completed consultation on its AI risk management policy in 2025.

Each is credible in isolation. For a CIO running cross-border ASEAN exposure, the consequence is immediate: stress scenarios, capital buffer calibrations and disclosure requirements are produced under different methodological assumptions in each market.

A bank with material Malaysian and Singaporean balance sheet exposure cannot generate a single consistent climate transition stress scenario when BNM and MAS calibrate the same underlying risk differently. Regulatory arbitrage is not a future concern. It is already priced into every cross-ASEAN book being run today.

The 13th AFMGM flagged climate risk management as a chairmanship priority. A supervisory convergence mechanism did not appear on the agenda.

The Deadline That Will Settle the Question

The Philippines holds the ASEAN chair through end-2026. Singapore takes over in 2027. The First Liveable, Equitable and Competitive Investor Forum is scheduled for 10-11 September 2026 in Manila. What gets committed there – and how much of it is construction-ready rather than pipeline – sets the terms Singapore inherits.

The Samarkand statement tasked deputies to advance the CMIM’s paid-in capital structure, the Disaster Risk Financing Initiative roadmap and the evolution of the Asian Bond Markets Initiative. Each requires domestic legislative follow-through before the regional framework produces instruments that move capital.

The ASEAN Finance Track has a consistent record on this sequence: directions endorsed regionally, implementation stalling nationally. The Philippines’ chairmanship has identified the right priorities across all three institutional layers: the safety net, the supervisory architecture and the green finance pipeline.

Closing the distance between a joint statement and a disbursed instrument – before the next shock renders the question moot – is what has not yet been demonstrated.

For fund managers and institutional investors with ASEAN exposure, September is the first real test. The pipeline figure tells you what was planned. The disbursement figure tells you whether the region’s financial architecture is moving at the speed of the risk it was designed to absorb.

References:

- Joint Statement of the 29th ASEAN+3 Finance Ministers’ and Central Bank Governors’ Meeting, Samarkand

- Joint Statement of the 13th ASEAN Finance Ministers’ and Central Bank Governors’ Meeting

- ADB’s Proposed USD 30 Billion Facility Among Key Outcomes of 13th AFMGM – Bernama

- ASEAN Catalytic Green Finance Facility 2025 Annual Report – Asian Development Bank

- ASEAN Catalytic Green Finance Facility – Overview – Asian Development Bank

- Central Banks Must Guide ASEAN+3 Through Age of Novel Risks – Aziz Durrani and Julia Anna Bingler, The Business Times / Green Central Banking

- Closing the Gap to Boost ASEAN Resilience Against Novel Risks – Julia Anna Bingler, Centre for Economic Policy

- ASEAN Finance and Central Bank Meetings Under Philippine Chairship – Philippine Information Agency

- 4th AMRO Forum: Deepen ASEAN+3 Integration for Resilience Amid Fragmentation – AMRO

{kind=link}